For anyone even thinking about building a custom home in Southwest Florida, the topic of hurricane insurance is sure to come up. It's a big one. You can expect premiums to fall somewhere between $4,000 to over $10,000 annually, even for brand-new, storm-resilient homes built with the latest features.

The final number on your policy isn't random; it's a direct reflection of your home's ability to stare down a hurricane and win. The core principle for any custom home builder in this market is simple: a stronger, smarter home built to modern codes with advanced hurricane impact features is going to be a whole lot cheaper to insure than an older property that's more of a gamble.

Understanding Your Insurance Costs in Southwest Florida

When you're building in places like Fort Myers or Cape Coral, your insurance premium isn't just another bill. It’s a scorecard for the design and construction choices you make. With the local insurance market under historic pressure, building for resilience has never been more important—or more financially rewarding. News affecting the building industry in Southwest Florida consistently points to a hardening insurance market, making resilient construction a financial necessity.

The sheer financial devastation from recent storms has completely changed the game for insurers. Hurricane Ian, for example, left behind an estimated $65 billion in insured losses, pushing many insurance companies to their limits. That one storm is a huge reason why premiums have shot up, especially right here in our coastal communities.

Key Factors in Premium Calculation

Think of an insurance underwriter as a professional risk assessor, meticulously inspecting your home's defenses. They're looking for anything and everything that could reduce potential damage when a storm hits. Here’s what they care about most in the custom home industry:

- Construction Quality: Solid concrete block homes paired with hurricane impact windows and doors are the gold standard for new builder trends. They're viewed far more favorably than older wood-frame houses, and your premium will reflect that.

- Roof Design and Age: A brand-new, hip-shaped roof is an engineer's dream for deflecting high winds. It offers far better resistance than a standard gable roof, and insurers will give you significant discounts for it.

- Building Elevation: This is a big one. How high your home sits in relation to the Base Flood Elevation (BFE) is critical. New design features often include elevated main floors, not just for views but for insurance savings. Building just a foot or two higher than required can slash your flood insurance costs—a separate but often mandatory policy. You can get a better feel for this by checking out the Fort Myers flood zone map and seeing how it affects properties.

- Hurricane Impact Features: A formal wind mitigation inspection is your ticket to savings. It officially verifies features like reinforced roof-to-wall connections and impact-rated garage doors, which translate directly into credits that lower your premium. Adding a whole-home generator in storms can also be seen as a risk-mitigation feature.

Estimated Annual Hurricane Insurance Premium Ranges in Southwest Florida

To put this all into perspective, here’s a look at how different types of homes might fare. This table gives a simplified overview of what you might expect to pay, showing just how much modern, resilient construction can save you year after year.

| Home Type | Estimated Annual Premium Range | Key Influencing Factors |

|---|---|---|

| New Custom Home (Resilient Construction) | $4,000 – $8,500 | Built to current codes, concrete block, impact windows, new hip roof, proper elevation, full wind mitigation credits. |

| Older Home (Pre-2002, Limited Mitigation) | $9,000 – $20,000+ | Wood-frame construction, older roof (especially gable), lower elevation, lacking modern storm shutters or impact-rated openings. |

As you can see, the difference is stark. The upfront investment in quality building materials and thoughtful design pays for itself over time through lower insurance costs.

The Foundation of Your Coverage

Before diving deep into hurricane-specifics, it helps to understand the basics. Getting familiar with the foundational parts of a standard policy is a great first step. This complete guide to a homeowners insurance policy does a great job of breaking down core concepts like liability, dwelling coverage, and personal property.

Ultimately, the best strategy for keeping your hurricane insurance costs in check is to work with a builder who doesn't just meet the minimum code but engineers homes to exceed it. That initial investment in a superior, hurricane-resistant home gives you more than just peace of mind—it delivers real, recurring savings for as long as you own it.

Why Florida's Insurance Market Is So Challenging

To really get why hurricane insurance costs in Florida are so high, you have to look back at the storms that came before. Today’s tough market wasn't created by a single bad year. It’s the product of decades of massive, landscape-altering hurricanes that have permanently changed how insurers calculate risk in the Sunshine State.

Every major storm leaves behind what we in the industry call a "hurricane tail"—a long-lasting financial hangover that keeps influencing premiums for years, sometimes decades, after the last gust of wind. It’s a compounding problem, where the staggering losses from one catastrophe pile on top of the next, making insurance carriers deeply cautious.

The Long Shadow of Past Storms

Imagine the Florida insurance market as a big savings account. During a few quiet years, insurers collect premiums and build up their reserves. But then a monster storm like Hurricane Andrew in 1992 comes along and makes a catastrophic withdrawal, wiping out all the gains and then some. This exact pattern has played out over and over again.

This isn’t just a theory; the numbers tell a brutal story. Since Hurricane Andrew caused $16 billion in insured losses, Florida insurers have racked up a cumulative net loss of $6.2 billion over nearly 30 years. After the flurry of eight storms in 2004 and 2005, the industry’s net worth crashed by -183.3% in 2004 and another -53.4% in 2005. It’s a perfect example of how one active season can obliterate years of financial stability. You can explore more data on this trend and see its direct impact on property insurance rates.

This history of devastating losses explains why insurers are so incredibly meticulous when they look at a property today, especially in a high-risk area like Southwest Florida. They aren’t just insuring your home for next season; they're betting against the combined financial weight of every major hurricane in the state’s modern history.

For insurance carriers, Florida is a uniquely volatile environment. The constant threat of high-category hurricanes forces their financial models to plan for the absolute worst-case scenarios. This makes them inherently conservative when writing new policies, particularly for coastal homes.

How History Shapes Modern Building Trends

This tough insurance landscape has directly pushed a massive shift in the custom home industry. Simply building to the minimum code is no longer good enough to get affordable—or any—coverage. Insurers are now demanding homes that are actively engineered to stand up to hurricane-force winds and storm surge, which is why you see so many new builders focusing on resilient design.

Here’s a direct line from past destruction to today’s best building practices:

- Concrete Over Wood: The catastrophic failure of older wood-frame homes in past hurricanes has made reinforced concrete block construction the gold standard for any insurable new home.

- Superior Roof Engineering: Insurance companies now give the best rates to homes with hip roof designs and advanced roof-to-wall connections. This is a direct lesson learned from watching countless gable roofs get peeled off like can lids in high winds.

- Elevated Living: The heartbreaking storm surge from storms like Ian hammered home the critical importance of elevation. Custom builders now design homes to sit well above the required Base Flood Elevation (BFE) to reduce flood risk and, in turn, lower insurance costs. This trend is central to new design features in Southwest Florida.

- Hardened Openings: Impact-rated windows, doors, and garage doors have gone from being luxury upgrades to absolute must-haves for securing a decent insurance policy.

At the end of the day, all this historical pressure has turned resilient design from a nice-to-have feature into a fundamental necessity. For anyone building a new custom home in Southwest Florida, understanding this history is crucial. It reframes the investment in hurricane-impact features and superior construction not as an extra expense, but as a direct and powerful strategy to make your home safe, secure, and—most importantly—insurable for the long haul.

The Anatomy of a Hurricane Insurance Premium

When an insurance underwriter looks at a new custom home in Southwest Florida, they don’t just see a beautiful building. They see a collection of risk factors. Every single piece—from the shape of your roof to the type of windows you choose—plays a part in calculating your final hurricane insurance premium.

If you’re building in Fort Myers or Cape Coral, you need to understand these factors. It's not just about safety; making smart design and material choices is one of the most direct ways to lower your insurance costs for years to come. This conversation about insurability is one you should have with your custom home builder long before you ever break ground.

Building Materials: Your First Line of Defense

The materials at the very core of your home's construction carry the most weight when determining your premium. After decades of storms, Florida insurers know exactly which materials hold up best under extreme stress. This is why solid concrete block construction is the preferred standard in our area—it’s proven to be resilient and earns homeowners significant insurance discounts.

On the other hand, traditional wood-frame homes, which are perfectly fine in other parts of the country, are seen as a much higher risk here. The potential for total failure from hurricane-force winds and driving rain means they will always cost more to insure. Choosing concrete block isn't just a building decision; it's a fundamental financial one.

Roof Design and Fortification

Right after the walls, the roof is the next thing an underwriter will scrutinize. It’s your home’s primary shield against a storm's power, and its design dramatically affects how it performs and how much you pay to insure it.

- Hip Roof vs. Gable Roof: A hip roof, which slopes down on all four sides, is naturally more aerodynamic and stable against high winds. Insurance companies love this design and reward it with big premium credits because it's far less likely to be ripped off by a major gust compared to a simple, two-sided gable roof.

- Roof-to-Wall Connections: How the roof structure is physically attached to the walls is just as crucial. Modern building codes mandate the use of strong metal connectors, often called hurricane straps or clips, that securely anchor the roof trusses to the home's concrete block walls. This reinforcement is a key feature checked during a wind mitigation inspection and prevents the roof from separating during a storm.

The Power of Wind Mitigation Credits

A wind mitigation inspection is basically a formal report card on your home’s hurricane-resistant features. You give this report to your insurance company to prove your home is built tough enough to handle high winds, which in turn unlocks some of the most valuable discounts you can get on your premium.

Think of a wind mitigation inspection as your chance to show the insurance company all the ways your custom home is "over-engineered" for safety. Every verified feature, from impact glass to a reinforced garage door, translates directly into a tangible credit that lowers what you pay every single year.

Here are the key features that earn you these critical credits:

- Opening Protection: This is all about your windows and doors. Hurricane-rated impact glass is designed and tested to withstand flying debris. This prevents a window from breaking, which would allow wind to rush inside and create catastrophic internal pressure that can blow the roof right off.

- Secondary Water Resistance (SWR): This is a special self-adhering membrane that goes on the roof deck before the shingles or tiles. It acts as a final waterproof barrier, stopping water from getting in even if the primary roofing material is torn away in a storm.

- Reinforced Garage Doors: Your garage door is often the largest and weakest opening in your home's exterior. A standard door can easily buckle under pressure. A hurricane-rated, reinforced garage door is absolutely essential for maintaining the structural integrity of your home and is a major source of insurance savings.

How Custom Home Features Impact Your Insurance Premium

The design and material choices you make with your builder have a clear and direct financial benefit. The table below breaks down how building for resilience from the start pays off.

| Feature | Standard Construction | Resilient Construction | Potential Insurance Impact |

|---|---|---|---|

| Wall Construction | Wood Frame | Reinforced Concrete Block | Significant Savings |

| Roof Shape | Gable Roof | Hip Roof | Significant Savings |

| Windows & Doors | Standard Glass | High-Impact Rated Glass | Major Savings |

| Roof Deck Protection | Standard Underlayment | Secondary Water Resistance (SWR) | Moderate Savings |

| Elevation | At or near Base Flood Level | Elevated 2+ Feet Above BFE | Lowers Flood Premium |

In the end, every decision matters. By focusing on these proven, hurricane-resistant features from the very beginning of the design process, you’re not just building a safer home—you’re engineering a more affordable one to insure right from the ground up.

How Smart Design Choices Lower Your Long-Term Costs

Building a custom home isn't just about getting the perfect layout; it's the single most powerful tool you have for controlling the long-term hurricane insurance cost Florida homeowners know all too well. When you invest in specific, "over-engineered" features that go way beyond the minimum code, you directly slash your insurance burden for as long as you own the home.

This strategy changes the game entirely. Your home transforms from a potential liability in an insurer's eyes into a fortified asset. It’s all about making smart decisions upfront that pay you back year after year through lower premiums, less risk, and priceless peace of mind when a storm starts churning in the Gulf.

Building Beyond the Code for Maximum Savings

In Southwest Florida, we see the minimum building code as just that—a minimum. True resilience, and the insurance savings that come with it, happens when a builder intentionally exceeds those standards. This is where features that might feel like upgrades are actually essential, long-term investments.

- Solid Concrete Block Walls: This is the backbone of a hurricane-ready home. Unlike wood-frame construction, reinforced concrete block walls offer incredible strength against brutal winds and flying debris, earning you a significant discount right off the bat.

- Superior Roof Tie-Downs: Modern engineering uses heavy-duty metal connectors, often called hurricane straps, to literally bolt the roof trusses directly to the concrete walls. This system prevents the roof from lifting off in extreme winds—a catastrophic failure that insurers heavily penalize.

- Elevated Foundations: Building your home's finished floor well above the required Base Flood Elevation (BFE) is a non-negotiable strategy. Every single foot of extra elevation can dramatically lower your separate flood insurance premium, which is a big deal in places like Cape Coral and Fort Myers.

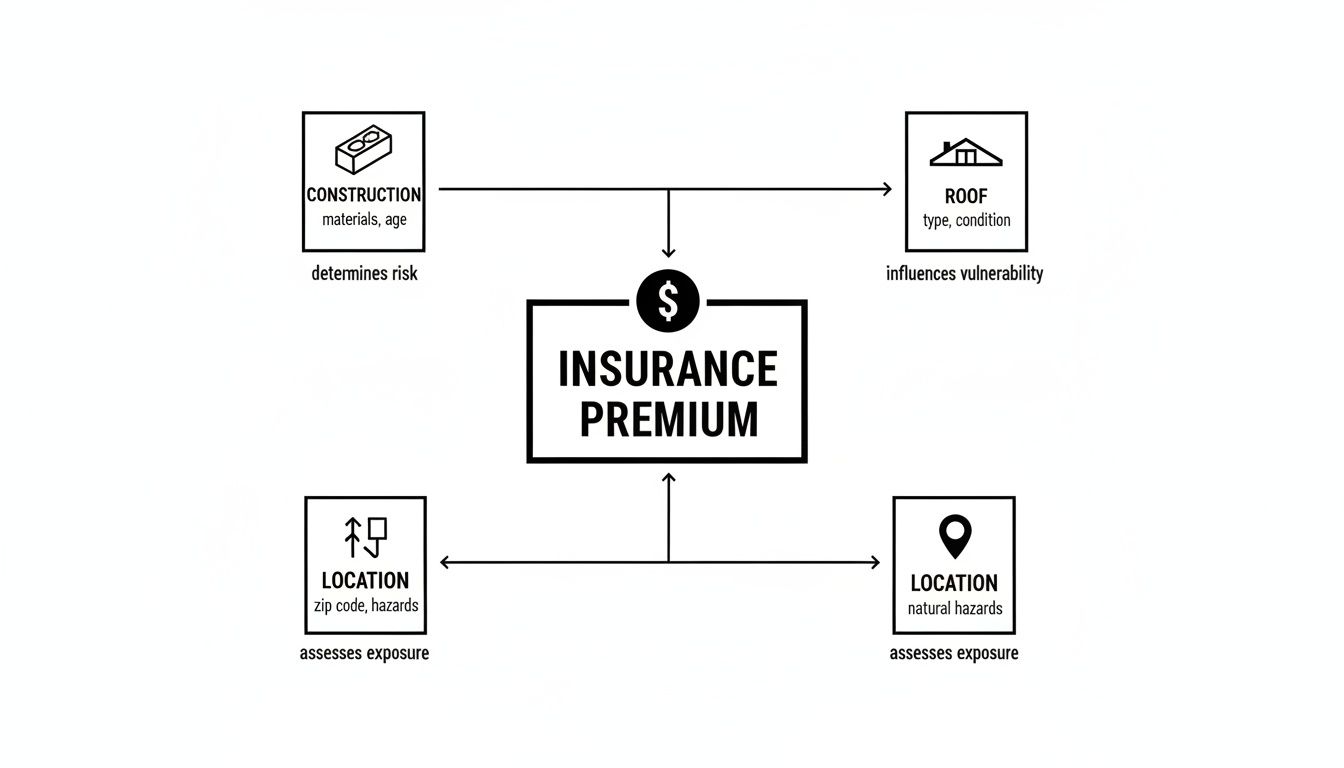

This diagram gives you a peek into how an insurer thinks, breaking down your home's risk into key areas that all add up to your final premium.

As you can see, your premium isn’t some random number based on your zip code. It's a direct result of the tangible choices made in construction, roofing, and where you site the home.

High-Tech Features That Insurers Reward

Beyond the core structure, today’s best custom homes include features that boost both safety and comfort while also cutting your insurance bill. These are the details that separate a standard new build from a truly resilient, and more affordable, custom home.

High-impact glass is a perfect example. These windows and doors are built with a tough laminated layer that holds the glass together even if it shatters, stopping wind and debris from blowing into your home. Preventing this kind of breach is a huge deal for insurers, and they'll reward you for it with serious premium credits. In fact, exploring the latest design ideas for new homes shows just how seamlessly you can blend top-tier safety with beautiful style.

Investing in high-quality, resilient construction is like pre-paying for your peace of mind. Every dollar spent on features like impact glass or a whole-home generator is an investment that lowers your annual insurance bill and protects your family during a storm.

The Unseen Value of a Whole-Home Generator

A whole-home generator probably isn't the first thing that comes to mind for insurance savings, but its impact is real. Of course, it provides comfort and keeps the lights on during an outage, but it also plays a key role in preventing secondary damage.

Think about it: after a storm, a long power outage in Florida's oppressive humidity is a recipe for a massive mold outbreak. That can lead to complicated, expensive insurance claims. By keeping the A/C running, a generator protects your home from that very threat. Insurers see this proactive move for what it is—smart risk management—and view a permanently installed generator as a feature that makes future claims less likely. That can absolutely have a positive effect on your overall risk profile and premium.

Hands-On Strategies to Manage Your Insurance Premiums

While the hurricane-resistant construction of your new Sinclair home is your single biggest advantage, you have more control over your insurance costs than you might think. Getting smart about your policy details is just as important as the reinforced concrete and impact glass protecting your family. Think of these steps as a financial toolkit—the perfect complement to the physical strength you've already built into your home.

Beyond the build itself, the way your policy is structured holds the key to major savings. The most direct lever you can pull is your deductible, but first, you have to understand a crucial detail about Florida insurance.

Master Your Deductibles

Here in Florida, you don’t have just one standard deductible. You actually have two, and they kick in for totally different reasons: a hurricane deductible and an "all other perils" (AOP) deductible.

- Hurricane Deductible: This one is a percentage of your home's insured value—typically 2%, 5%, or 10%—and it only applies to damage from a named storm. On a $700,000 home, a 2% deductible means you’re on the hook for the first $14,000 in repairs.

- AOP Deductible: This is a simple flat dollar amount, like $1,000 or $2,500, that covers everything else that could happen, like a kitchen fire or a theft.

Here’s the strategy: opting for a higher hurricane deductible, say 5% instead of 2%, will dramatically lower your yearly premium. It’s a calculated trade-off. You agree to take on more financial risk if a hurricane hits in exchange for significant savings every single year. For a modern, well-built custom home designed to shrug off storms, that’s a bet that can really pay off.

By strategically increasing your hurricane deductible, you are essentially betting on your home's superior construction. You're telling the insurer that you believe in the resilient features you’ve invested in, and in return, they reward you with a lower premium.

Find a Specialist and Review Annually

The insurance market in Florida is a tangled web, and it’s always changing. This is why working with an independent insurance agent who specializes in Southwest Florida is non-negotiable. Unlike a "captive" agent who only sells for one company, an independent agent can shop your policy around to find the absolute best fit for your high-value custom home.

And it’s not a one-and-done deal. Your insurance needs can shift, so a yearly policy review with your agent is essential. This check-up ensures your coverage still matches your home's value and lets you jump on any new discounts or market changes that could drop your premium. Pro tip: bundling your home and auto policies with the same company almost always unlocks extra savings.

Finally, being proactive is great, but you also need to be ready if you ever have to make a claim. Taking the time now to understand how to fight your insurance company for a hurricane claim settlement is a critical piece of the puzzle. Having that knowledge in your back pocket can make a stressful situation a whole lot smoother.

Building Your Secure and Insurable Dream Home

Navigating Florida's insurance market can feel overwhelming, but the way forward is simpler than you might imagine. While the hurricane insurance cost Florida residents pay is a real concern, building a new custom home gives you the single greatest advantage in controlling that cost for years to come.

It really boils down to this: proactive, resilient design is your best financial strategy.

This mindset changes the conversation from merely building a house to engineering a secure, financially sound asset. The decisions you make at the very start of the design phase ripple through your annual premiums for as long as you own the home. It’s not something to think about later—it’s a foundational piece of your home's financial blueprint.

Partnering With Your Builder for a Smarter Build

Bringing your builder into the conversation early is non-negotiable. This is when you can talk through how specific design choices and materials will directly translate into insurance savings. Every decision, from the type of block used in the walls to the shape of the roof, is an opportunity to lower your risk profile and, in turn, your premium.

A builder who truly knows the Southwest Florida insurance landscape can be your guide. They can show you the long-term ROI of investing in features that go above and beyond the minimum building code, ensuring your home is built not just to be safe, but to be highly insurable. To see how these critical talks fit into the bigger picture, you can review the stages of the custom home building process and see where these conversations naturally take place.

The most effective way to manage your insurance costs is to build a home that insurers want to cover. By focusing on resilience from day one, you shift from being a high-risk applicant to a preferred client, unlocking the best possible rates for your beautiful new home.

Essential Resources for Florida Homeowners

Building a home that’s both stunning and insurable requires having the right information at your fingertips. Here are a few key resources to get you started on the right foot:

- Check FEMA Flood Maps: Before you even fall in love with a lot, understand its flood risk. Use the official FEMA maps to check the Base Flood Elevation (BFE) for the property. This single piece of data will dictate your foundation design and heavily influence your flood insurance costs.

- Find a Local Insurance Specialist: Don't just get a generic quote online. You need to partner with an independent insurance agent who specializes in high-value coastal properties right here in Fort Myers and Cape Coral. They work with the right carriers and know the ins and outs of insuring a new custom home in this area.

- Prioritize a Wind Mitigation Inspection: As soon as construction wraps up, make sure your builder provides all the necessary paperwork for a wind mitigation inspection. Think of this report as your golden ticket—it’s what officially unlocks the maximum discounts you’ve earned for all of your home’s hurricane-resistant features.

Frequently Asked Questions About Florida Hurricane Insurance

Let's cut right to it. Here are some of the most common questions we get about insuring a new custom home in Southwest Florida. We'll give you straight answers to help you make sense of the state's tricky insurance market.

Does a Brand New Roof Guarantee a Lower Premium?

Absolutely. In fact, a new roof is one of the single biggest levers you can pull to lower your insurance premium. Insurers see older roofs as a massive liability, and they price policies accordingly.

For a new custom home, combining a hip roof design with a secondary water resistance (SWR) layer is the gold standard. This setup qualifies for the maximum wind mitigation credits, leading to serious savings compared to homes with other roof types.

What Is the Difference Between Flood and Hurricane Insurance?

This is a critical distinction that every Florida homeowner needs to get right. Your standard homeowner's policy covers damage from wind—that's your hurricane coverage. It absolutely does not cover damage from rising water or storm surge.

Flood insurance is a completely separate policy, most often purchased through the National Flood Insurance Program (NFIP). If your home has a mortgage and is in a designated flood zone, it's mandatory. When you're building in places like Cape Coral or Fort Myers, you have to budget for both policies to be fully protected. It's non-negotiable.

Can I Still Get Insurance from Major National Companies?

It's tough. Florida’s challenging market has pushed many of the big national insurance carriers to pull back, especially in high-risk coastal areas. They simply aren't writing new policies here anymore. This is exactly why working with a local, independent insurance agent is so important when building a new home.

An independent agent isn't locked into one company. They have connections to a whole network of carriers, including smaller Florida-based insurers and specialty lines. They know this market inside and out and can shop around to find the best possible coverage for your new property.

How Much Does Building Elevation Affect Insurance Costs?

It’s a huge deal, specifically for your flood insurance policy. Building your home's finished floor just a foot or two above the required Base Flood Elevation (BFE) can slash your flood insurance premiums for the entire life of the home.

This isn't a small decision—it's one of the most important financial conversations you'll have with your custom builder during the design phase. A little extra height upfront can save you thousands over the long run.

At Sinclair Custom Homes Inc, we don’t just build beautiful homes; we engineer them to be safe, resilient, and highly insurable. We build smart from the ground up, integrating design choices that deliver both peace of mind and lasting financial benefits. Start planning your secure and insurable dream home with us today.